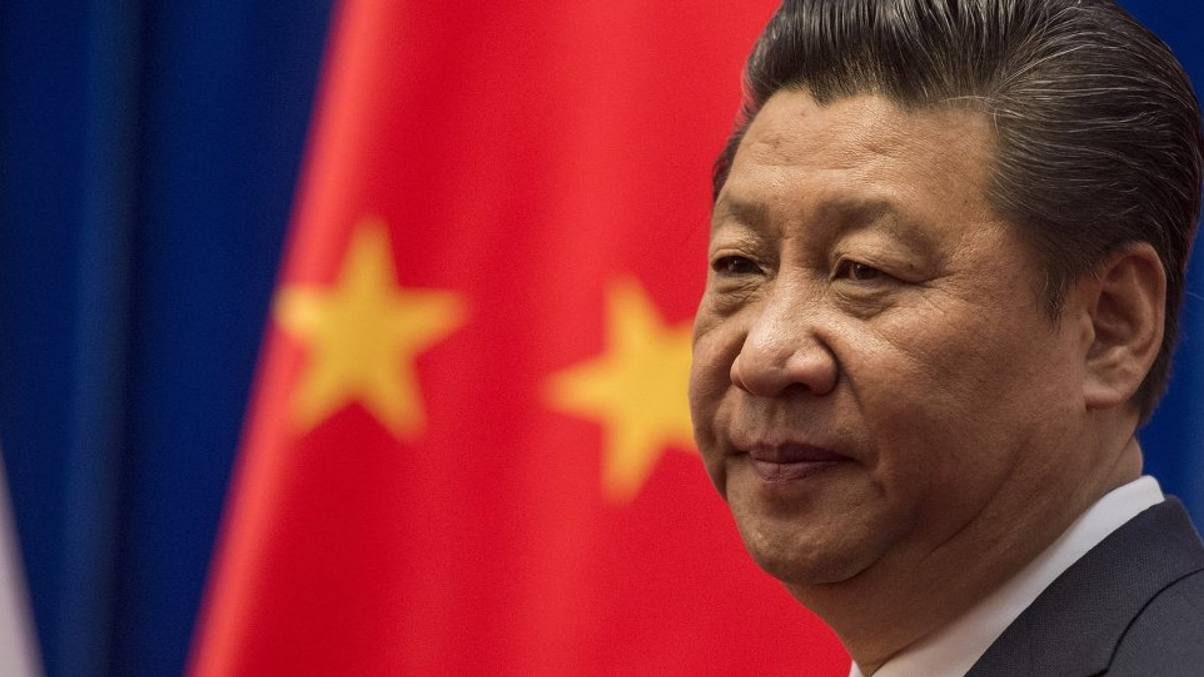

Xi Jinping’s term limit drop sparks long-term uncertainty

Scrapping the two term limit for China's president will usher in more political stability, say foreign investors. But there are long term risks they need to be aware of.

Foreign investors appear relaxed about China’s proposed constitutional amendment to the president’s two term limit, but political experts believe the move could engender more uncertainty over the longer term.

Sign in to read on!

Registered users get 2 free articles in 30 days.

Subscribers have full unlimited access to AsianInvestor

Not signed up? New users get 2 free articles per month, plus a 7-day unlimited free trial.

¬ Haymarket Media Limited. All rights reserved.