Bonds are dead: GMO

“I am well aware of the dangers of proclaiming the death of an asset class,” says James Montier at GMO, who does so anyway, advising higher cash holdings.

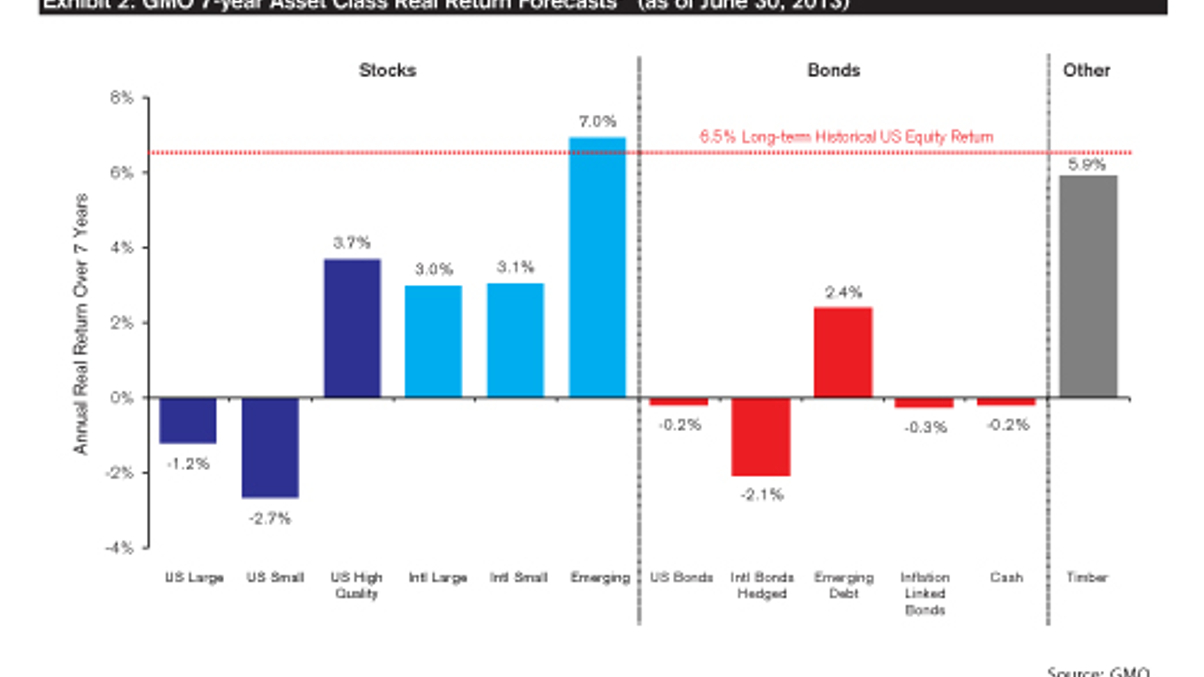

The lack of value in fixed income is rendering the asset class useless to investors, argues James Montier, a strategist at GMO.

Sign in to read on!

Registered users get 2 free articles in 30 days.

Subscribers have full unlimited access to AsianInvestor

Not signed up? New users get 2 free articles per month, plus a 7-day unlimited free trial.

¬ Haymarket Media Limited. All rights reserved.